Oil futures prices are below $38 but there is a glimmer of hope in EIA’s Short-Term Energy Outlook (STEO) released today–world consumption increased in November and supply fell.

OPEC did what everyone expected last week–nothing–and oil markets reacted badly. Brent futures fell 15% from $47.44 before the OPEC meeting on Friday (December 4) to $40.25 today (December 8). I have been saying that oil prices have been too high based on fundamentals and need to move lower in order for oil markets to balance.

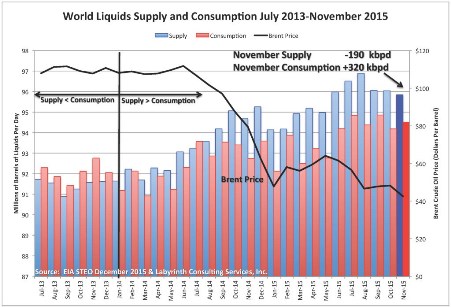

Now we may be seeing the beginnings of that trend. In November, world liquids supply fell 190,000 bpd and consumption increased 320,000 bpd (Figure 1).

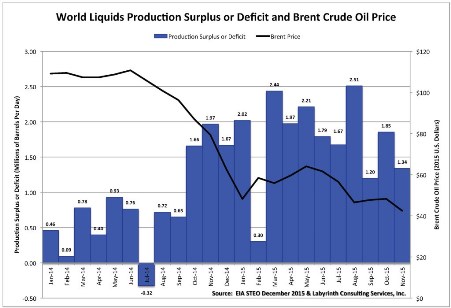

That lowers the production surplus (supply minus consumption) to 1.34 million bpd (Figure 2) which is not great but is a big improvement–a 520,000 bpd decrease–over October and is one of the better months of 2015.

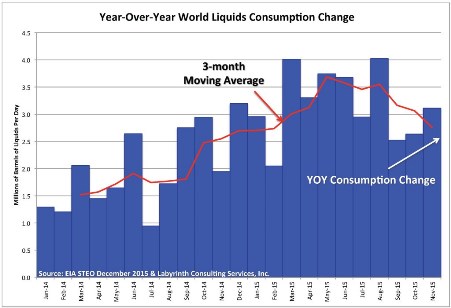

Most analysts are focused on the over-supply but I worry more about demand. Lower prices have forced producers to cut back and world production has been falling for the last 4 months. Demand is a tougher problem because people have to change their behavior and use more oil. Consumption is not the same as demand but it is a proxy and has increased year-over-year for 3 consecutive months (Figure 3) despite the medium-term downward trend (3-month moving average).

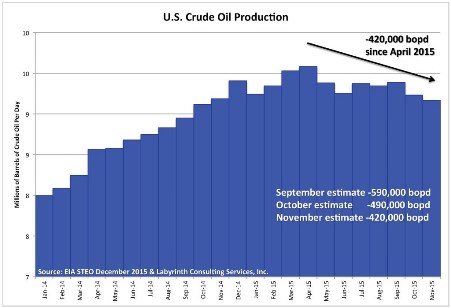

Although U.S. production continues to decline, the EIA has revised the amount of decrease downward over the past 2 months (Figure 4).

U.S. production has declined 420,000 bopd since April but last month’s estimate was -490,000 bopd and the September estimate was -590,000 bopd. Although U.S. production is important, it alone will not fix the world supply surplus. At the same time, I expect it will continue to decline and EIA forecasts a decrease of 1.12 million bopd by September 2016.

It is too early for optimism. The global market remains over-supplied by 1.3 million bpd and a few months do not necessarily make a trend. At the same time, with prices now below $40 per barrel, I am encouraged that there is the potential for progress toward market balance and eventual price recovery.

This article originally appeared on Oilprice.com

More from Oilprice.com:

More Must-Reads from TIME

- Donald Trump Is TIME's 2024 Person of the Year

- Why We Chose Trump as Person of the Year

- Is Intermittent Fasting Good or Bad for You?

- The 100 Must-Read Books of 2024

- The 20 Best Christmas TV Episodes

- Column: If Optimism Feels Ridiculous Now, Try Hope

- The Future of Climate Action Is Trade Policy

- Merle Bombardieri Is Helping People Make the Baby Decision

Contact us at letters@time.com