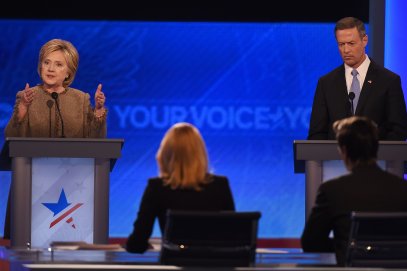

Clinton Hits Back at O'Malley Over Wall Street Donations

Martin O’Malley hit Hillary Clinton over an answer — from the last debate.The former Maryland governor criticized Clinton for her ties to Wall Street, bringing up her response to a question on the topic at...

By Maya Rhodan