---

title: Jacob Davidson | TIME

description: Breaking news and analysis from time.com. Politics, world news, photos, video, tech reviews, health, science, and entertainment news.

canonical: https://time.com/author/jacob-davidson/

og:title: TIME | Current & Breaking News | National & World Updates

og:description: Breaking news and analysis from time.com. Politics, world news, photos, video, tech reviews, health, science, and entertainment news.

og:url: https://time.com/author/jacob-davidson/

og:site_name: TIME

og:image: https://static.time.com/v3/assets/bltea6093859af6183b/bltde093bcdab65f2d0/6988d9b9bc6cfc69913e2a3c/time-logo.jpg?branch=production

og:image:width: 300

og:image:height: 300

og:image:alt: Breaking news and analysis from time.com. Politics, world news, photos, video, tech reviews, health, science, and entertainment news.

og:type: profile

twitter:card: summary

twitter:title: TIME | Current & Breaking News | National & World Updates

twitter:description: Breaking news and analysis from time.com. Politics, world news, photos, video, tech reviews, health, science, and entertainment news.

twitter:image: https://static.time.com/v3/assets/bltea6093859af6183b/bltde093bcdab65f2d0/6988d9b9bc6cfc69913e2a3c/time-logo.jpg?branch=production

---

# Jacob Davidson

## Jacob Davidson

## Jacob Davidson

*

Jun 16, 2016

### [Why Jo Cox's Shooting Is So Shocking for Britain](https://time.com/4371945/jo-cox-shooting-england-gun-control/)

England is known for its tight gun laws and very low rates of gun violence

[WORLD](/section/world/)

*

Jun 16, 2016

### [Why This Tech Company Is Giving 100 People Free Money](https://time.com/4369209/universal-basic-income-y-combinator/)

Startup accelerator Y Combinator is testing a Universal Basic Income, in which people get money to s...

[BUSINESS](/section/business/)

*

Jun 13, 2016

### [The Las Vegas Shooting Is a Haunting Reminder of Just How Many Guns Are in America](https://time.com/4188456/orlando-shooting-mass-shootings-gun-control/)

The U.S. has more firearms than any other country in the world.

[U.S.](/section/us/)

*

Apr 28, 2016

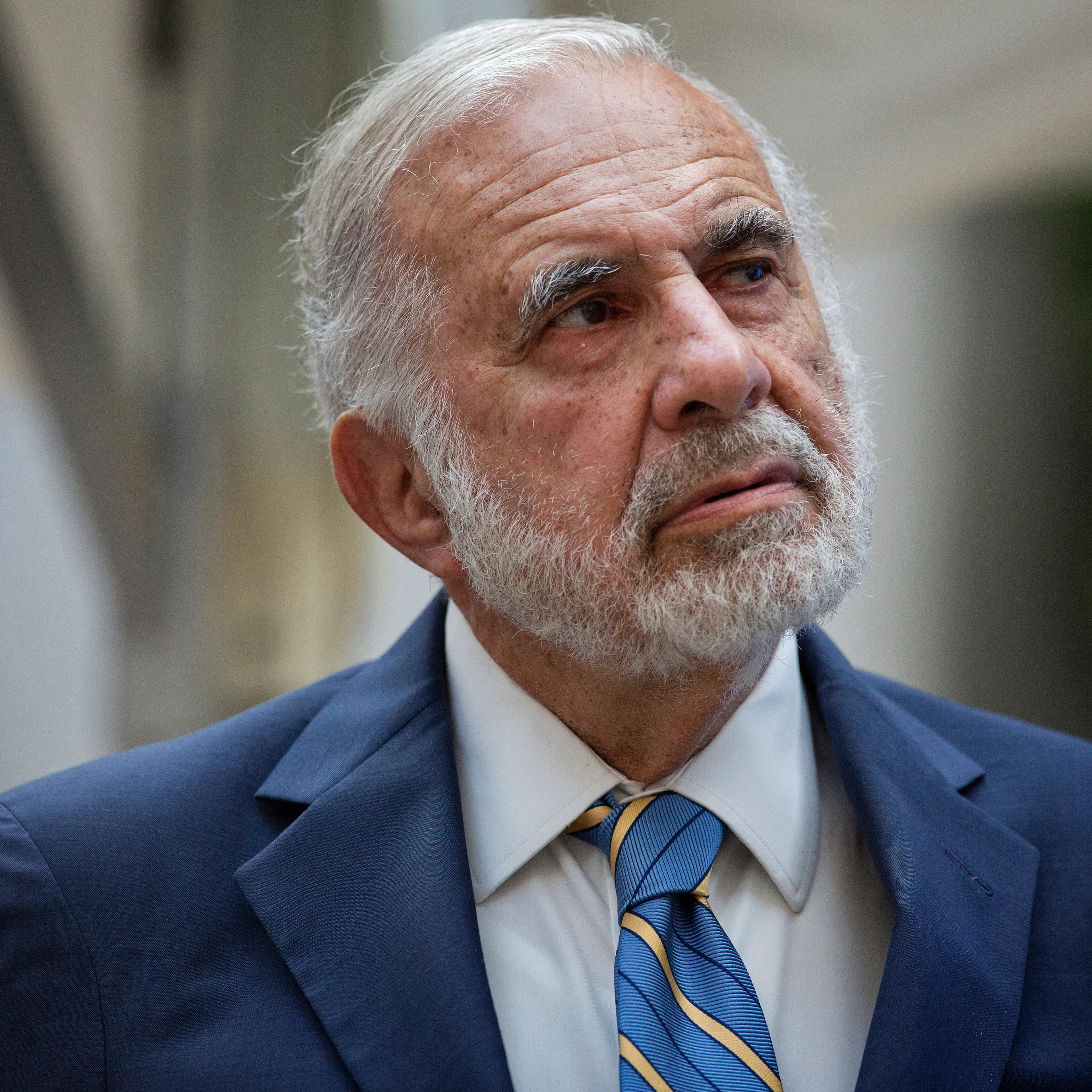

### [Carl Icahn Bails on Apple](https://time.com/4311572/carl-icahn-sells-apple-stock/)

He's worried about Apple's relationship with China

[BUSINESS](/section/business/)

*

Apr 11, 2016

### [7 Easy Ways To Get Your Financial Life in Order](https://time.com/4285164/financial-health-checklist/)

Use this simple financial health checklist

*

Mar 25, 2016

### [The Unsettling Truth About America's Economic Recovery](https://time.com/4269733/secular-stagnation-larry-summers/)

Why hasn't America's economy recovered more robustly? Economists have an unsettling answer

[BUSINESS](/section/business/)

*

Feb 12, 2016

### [How to Watch All the TV You Want Without Paying a Cable Bill](https://time.com/4119383/cable-tv-without-paying-bill/)

Here are five ways to ditch cable—and save hundreds of dollars in the process

*

Feb 11, 2016

### [America's Debt Isn't the Crisis People Think](https://time.com/4214269/us-national-debt/)

The answer from most economists may surprise you

[BUSINESS](/section/business/)

*

Jan 9, 2016

### [Canada PM Condemns Pepper Spray Attack on Refugees](https://time.com/4174198/justin-trudeau-pepper-spray-syria-refugee/)

"This isn't who we are"

[WORLD](/section/world/)

*

Jan 9, 2016

### [Silent Muslim Protester Kicked Out of Donald Trump Rally](https://time.com/4174182/muslim-protester-donald-trump-rally/)

She wore a blue T-shirt saying 'Salam, I come in peace'

[POLITICS](/section/politics/)

*

Dec 21, 2015

### [The U.S. Government's Finance Watchdog Gets Ready for 2016](https://time.com/4157558/mary-jo-white/)

How Mary Jo White is looking to the year ahead

[POLITICS](/section/politics/)

*

Dec 1, 2015

### [A Criminologist's Case Against Gun Control](https://time.com/4100408/a-criminologists-case-against-gun-control/)

A law professor explains why he is skeptical about new approaches to gun violence in America

[IDEAS](/section/ideas/)

*

Nov 19, 2015

### [7 Fascinating Letters From the Time Inc. Archives](https://time.com/4118122/letters-from-time-archive/)

From the desks of Winston Churchill, Joseph McCarthy, John F. Kennedy and more

[HISTORY](/section/history/)

*

Nov 19, 2015

### [The Most Amazing Artifacts From the TIME Archives](https://time.com/4116950/amazing-historical-artifacts-from-time/)

Highlighting some of the most special items from the century-spanning collection

[WORLD](/section/world/)

*

Oct 28, 2015

### [Israel Struggles With How to Thwart a Viral 'Instafada'](https://time.com/4088474/israel-facebook-kife-attacks-social-media-terrorism/)

Violence spreading by social media has put Facebook in the spotlight in Israel

[WORLD](/section/world/)

Meta: null

```json

[{"@context":"https://schema.org","@type":"Organization","@id":"https://time.com/","name":"TIME","url":"https://time.com/","logo":{"@type":"ImageObject","url":"https://time.com/images/logo.png","width":528,"height":156},"foundingDate":"March 3, 1923","sameAs":["https://www.facebook.com/time","https://www.instagram.com/time/?hl=en","https://twitter.com/time","https://www.pinterest.com/timemagazine"]},{"@context":"https://schema.org","@type":"BreadcrumbList","itemListElement":[{"@type":"ListItem","position":1,"item":{"@id":"https://time.com/","name":"Home"}},{"@type":"ListItem","position":2,"item":{"@id":"https://time.com/author/jacob-davidson/","name":"Jacob Davidson"}}]},{"@context":"https://schema.org","@type":"Person","@id":"https://time.com/author/jacob-davidson/","mainEntityOfPage":{"@type":"WebPage","@id":"https://time.com/author/jacob-davidson/"},"name":"Jacob Davidson","jobTitle":null,"description":"","url":"https://time.com/author/jacob-davidson/","worksFor":{"@type":"Organization","name":"TIME","url":"https://time.com/"}}]

```