Let’s get the good news out there first: Yes, the U.S. has finally, after four years of recovery, exceeded its pre-recession jobs peak of 138.4 million new jobs. There are now more jobs out there in the economy than ever before, though it’s worth saying there are also a lot more people in the labor market than there were back then, even given the historically low workforce participation rate of 62.8 percent (the lowest since 1979).

The big question is “who are those jobs for?” That’s where the May jobs report, the fourth strong report in a row, gets more interesting. Unlike previous reports, the gains have been broad based—there were new jobs created in many sectors, including higher paying and important ones like manufacturing and construction. But 50% of all the jobs being created in this country are still in the low-wage category—retail clerk positions, home heath aids, waitresses and the like. And more importantly, pay isn’t going up much—only a little more than 2% month on month, compared to an average of 3.5% to 4.5% before the recession. If you aren’t jumping up and down about this report, that’s probably why—a lot of us just don’t feel the recovery in our pocketbooks.

When Paul and Ieva Johnson moved from Minnesota to Florida, they were looking forward to warm weather and plenty of bargain-priced homes. But when the couple made their first offer earlier this year, they quickly discovered that they'd have to settle for the sunshine.

Not only didn't they get the house, says Paul, but "we didn't even get a callback." Over the next two months they put in seven offers -- most at or above asking price -- before finally making a successful $365,000 bid on a Sarasota three-bedroom.

To their surprise, buyers in some housing markets are finding that they're no longer in the power position. The reason is simple: too many bidders and not enough homes.

A growing number of shoppers are on the hunt, confident that the market has hit bottom, say brokers. Yet many would-be sellers are staying on the sidelines, either because they're underwater or because prices are still painfully low.

Related: Best home deals in the Best Places to Live

In June the number of houses listed for sale nationwide dropped 24% compared with the year prior, sending the supply of homes relative to buying activity down to levels not seen since 2006.

That's led to some stiff competition among buyers, says Sin-Yi Chao Lambertson, a broker in Glendora, Calif.: "I've had listings get 45 offers."

As the economy improves, the supply of homes should bounce back. If you're in the market now, though, and want to ensure yours is the winning bid, take these steps:

Size up your town. First you'll need to determine whether you could be in for a bidding war. Rising price tags are a sign that sellers are gaining ground, but prices often lag the market.

Related: Buy or rent? 10 major cities

Two other stats, available on real estate site Zillow, can mean an area's heating up: a drop in the percentage of homes with list price cuts, and an increasing ratio of sales to asking prices.

Don't skimp on credit. With many sellers worried about deals falling through, you'll need the bank's blessing right away. Don't waste time on prequalification, which is an estimate of how much you might be able to borrow.

"When multiple offers come in, I'll toss out anything that's just prequalified," says Teri Herrera, a broker in Redmond, Wash. Pre-approval based on your credit, income, and assets is better, and full credit approval, which goes through the bank's underwriting department, is best.

Get a veteran on your side. Finding an experienced agent is even more important in a competitive market; you'll want a pro who specializes in working with buyers and who knows the local players and pricing trends.

"One of your first questions should be whether the agent has experience in multiple-offer situations," says Herrera, adding that it's also important to get details on the deals she's closed recently. A good agent can help you determine whether a home is fairly priced, advise you on how much to offer -- and back up her counsel with data and examples.

Make a clean offer. When you take the leap, remember that "the best offer isn't always the one with the best price," says George Miller, the Johnsons' Sarasota agent. "It's the one with the fewest hassles and outs for the buyer."

Make yours as straightforward as possible. If it's contingent on selling an existing home, for example, you're unlikely to win a bidding war. Set on a certain closing date? Consider whether it's worth blowing the deal. In this market, the answer is probably no.

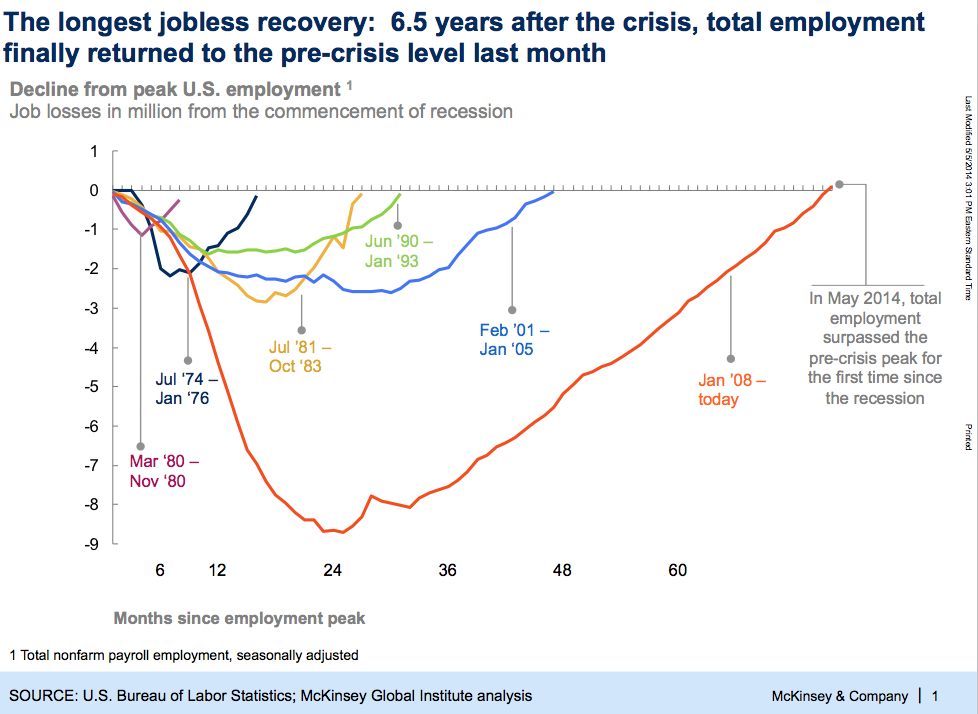

That’s underscores the key difference in the pre-2008 economy versus now. Yes, the jobs debate has officially shifted from quantity, to quality. But, as the McKinsey Global Institute has been pointing out for some time now, that shift has taken longer than in any recovery of the past. From the period between World War II and the 1980s, “there was a fairly predictable pace for recoveries,” says MGI director and economist Susan Lund. It took roughly six months for U.S. employment levels to recover after each post-war recession through the 1980s. Then, things changed. It took 15 months after the 1990–91 recession for employment to reach its pre-crisis levels, and 39 months after the 2001 recession. This time around, it’s taken 40 months, and $4 trillion of Federal Reserve stimulus to boot.

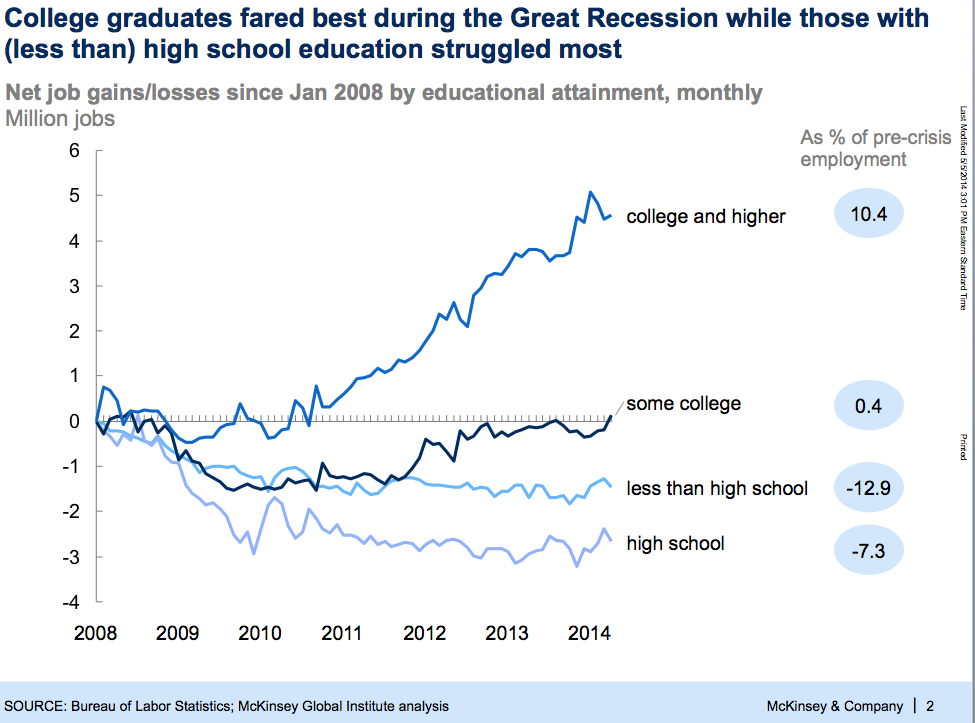

What’s more, while we’ve created as many jobs as we had before, the nature of the work has changed—the labor market is bifurcated, with people at the top doing quite well and those in the middle and bottom, not so much. Another fascinating tidbit from MGI that reflects this shift: employment for people with a bachelor’s degree or more has actually been growing since the crisis in 2008. It never stopped growing. But work for those with a high school degree or less has been shrinking, and only just began to rebound. “For those people, it still feels like a jobless recovery.”

When Paul and Ieva Johnson moved from Minnesota to Florida, they were looking forward to warm weather and plenty of bargain-priced homes. But when the couple made their first offer earlier this year, they quickly discovered that they'd have to settle for the sunshine.

Not only didn't they get the house, says Paul, but "we didn't even get a callback." Over the next two months they put in seven offers -- most at or above asking price -- before finally making a successful $365,000 bid on a Sarasota three-bedroom.

To their surprise, buyers in some housing markets are finding that they're no longer in the power position. The reason is simple: too many bidders and not enough homes.

A growing number of shoppers are on the hunt, confident that the market has hit bottom, say brokers. Yet many would-be sellers are staying on the sidelines, either because they're underwater or because prices are still painfully low.

Related: Best home deals in the Best Places to Live

In June the number of houses listed for sale nationwide dropped 24% compared with the year prior, sending the supply of homes relative to buying activity down to levels not seen since 2006.

That's led to some stiff competition among buyers, says Sin-Yi Chao Lambertson, a broker in Glendora, Calif.: "I've had listings get 45 offers."

As the economy improves, the supply of homes should bounce back. If you're in the market now, though, and want to ensure yours is the winning bid, take these steps:

Size up your town. First you'll need to determine whether you could be in for a bidding war. Rising price tags are a sign that sellers are gaining ground, but prices often lag the market.

Related: Buy or rent? 10 major cities

Two other stats, available on real estate site Zillow, can mean an area's heating up: a drop in the percentage of homes with list price cuts, and an increasing ratio of sales to asking prices.

Don't skimp on credit. With many sellers worried about deals falling through, you'll need the bank's blessing right away. Don't waste time on prequalification, which is an estimate of how much you might be able to borrow.

"When multiple offers come in, I'll toss out anything that's just prequalified," says Teri Herrera, a broker in Redmond, Wash. Pre-approval based on your credit, income, and assets is better, and full credit approval, which goes through the bank's underwriting department, is best.

Get a veteran on your side. Finding an experienced agent is even more important in a competitive market; you'll want a pro who specializes in working with buyers and who knows the local players and pricing trends.

"One of your first questions should be whether the agent has experience in multiple-offer situations," says Herrera, adding that it's also important to get details on the deals she's closed recently. A good agent can help you determine whether a home is fairly priced, advise you on how much to offer -- and back up her counsel with data and examples.

Make a clean offer. When you take the leap, remember that "the best offer isn't always the one with the best price," says George Miller, the Johnsons' Sarasota agent. "It's the one with the fewest hassles and outs for the buyer."

Make yours as straightforward as possible. If it's contingent on selling an existing home, for example, you're unlikely to win a bidding war. Set on a certain closing date? Consider whether it's worth blowing the deal. In this market, the answer is probably no.

Increasingly, though, the question is whether it will be a wage-less recovery. It usually takes several months of job growth for income to start to pick up, and once it does, it’s possible that a broader range of companies will start adding more employees higher up the food chain. The National Association of Business Economists is bullish on the next six months. But I tend to think that even as jobs will grow, these key trends— the shrinking of the middle labor market, and flat wages—will continue. One of the main reasons could be that technology related job destruction is continuing in blue chip America, and it’s going higher up the food chain. I recently sat in on a conference with a high level group of C-suite employers, and all were planning to spend on technology that would displace more white-collar workers. Research shows the only way to shift that trend is to increase levels of education in society faster than technology change—and given the speed at which the latter is advancing, that will be a tough assignment indeed.