{kind=link}

{kind=link}

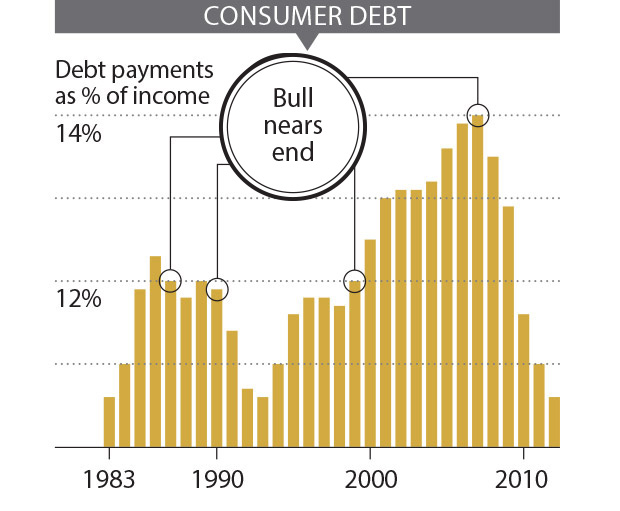

As investor confidence grows, overspending and overborrowing are typically byproducts of an aging bull market. Since the financial crisis ended, though, prudence has been in fashion. That, combined with record low interest rates, has pushed average household monthly debt payments as a percentage of disposable income to the lowest level since the 1990s. Should the economy improve, consumers have the means to ramp up spending.

Another gauge of exuberance is housing starts. Last year the number of new homes being constructed in the U.S. rose sharply as the real estate market finally began to stabilize. But annual housing starts were still only about half the long-term average. Says Stephen Auth, chief investment officer of equities at Federated Investors: “We’re not even getting going yet.”