TIME logo

Sign In

My Account

My Account

Digital Magazines

TIME Storefront

Help Center

Sign Out

Subscribe

Subscribe

Sign Up for Our Entertainment Newsletter

Close

My Account

My Account

Digital Magazines

TIME Storefront

Help Center

Sign Out

Sign In

Subscribe

Sections

Home

U.S.

Politics

World

Health

Climate

Future of Work by Charter

Business

Tech

Entertainment

Ideas

Science

History

Sports

Magazine

TIME 2030

Next Generation Leaders

TIME100 Leadership Series

TIME Studios

Video

TIME100 Talks

TIMEPieces

The TIME Vault

TIME for Health

TIME for Kids

TIME Edge

TIME CO2

Red Border: Branded Content by TIME

Coupons

Personal Finance by TIME Stamped

Shopping by TIME Stamped

Join Us

Newsletters

Subscribe

Give a Gift

Shop the TIME Store

TIME Cover Store

Customer Care

US & Canada

Global Help Center

Reach Out

Careers

Press Room

Contact the Editors

Media Kit

Reprints and Permissions

More

About Us

Privacy Policy

Your Privacy Rights

Terms of Use

Modern Slavery Statement

Site Map

Connect with Us

Recession

Hundreds Arrested in Venezuela Food Riots

By Rishi Iyengar

These 5 Facts Explain the Unstable Global Middle Class

By Ian Bremmer

Study: Public University Tuition Way Up Since Recession

By Claire Groden / Fortune

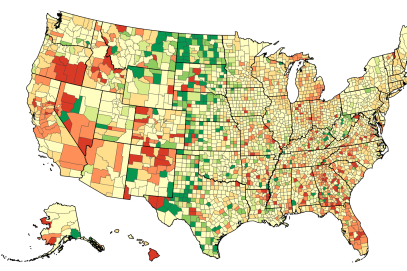

See How Well Your Neighbors Have Recovered From the Recession

By Chris Wilson

More in

Recession

Europe Could Derail America's Economic Recovery

Central banks around the world are moving in different directions

By Rana Foroohar

December 3, 2015

Hillary Owned Bernie Last Night on Finance

Focusing on shadow banking was a deft move that neither alienated her supporters nor skirted real issues

By Rana Foroohar

October 14, 2015

Emerging Headache: Brazil Sinks Deeper Into Recession

Poor government policy, slowing demand for natural resources to blame

By Chris Matthews / Fortune

September 25, 2015

How to Understand the Global Impact of China's Impending Slowdown

What happens in Beijing doesn't stay in Beijing

By Ian Bremmer

August 28, 2015

More Bad Data From China Triggers a Global Selloff

New report shows the country's manufacturing sector continuing to contract

By Chris Matthews / Fortune

August 21, 2015

This Surprising Area Is Seeing Significant Job Growth

Good news for college graduates.

By Michal Addady / Fortune

August 18, 2015

Parents Are Shelling Out More Money For Kids to Attend College

More financing from the Bank of Mom and Dad

By Claire Groden / Fortune

July 21, 2015

Rising Birth Rates a Good Sign for the Economy

First increase since the recession

By Josh Sanburn

June 17, 2015

Most Americans Say Wealth Inequality Is a Huge Issue

Expect it to be a 2016 campaign theme

By Claire Zillman / Fortune

June 4, 2015

The Left's Opening Gambit for 2016 Is All About Your Paycheck

The unifying value for progressives in 2016? Wages, if leaders like Elizabeth Warren and Richard Trumka have anything to say about it

By Rana Foroohar

January 6, 2015

Utah Abortion Rate Lowest Ever

Restrictive abortion laws, economics and the increased availability of contraceptives could all be behind the trend

By Helen Regan

December 29, 2014

U.S. Sells Off Last Major TARP Investment, 6 Years On

U.S. taxpayers made around $2.4 billion in the Ally investment

By Alex Rogers

December 19, 2014

Five Best Ideas of the Day: December 15

1. To head off surging antimicrobial resistance — which could claim 10 million lives a year by 2050 — we need new drugs and better rules for using the ones we have.By Fergus Walsh at...

By The Aspen Institute

December 15, 2014

Wealth Gap Widens Between Whites and Minorities

The gap between white and black household wealth is the highest since 1989

By Denver Nicks

December 12, 2014

Millennials Worse Off Than Parents

The latest Census numbers show Americans aged 18 to 34 struggling worse than their parents did in the '80s

By Josh Sanburn

December 4, 2014

Japan Sinks Into Recession (Again)

An unexpected contraction in quarterly GDP shows that Prime Minister Shinzo Abe’s radical economic program is badly broken

By Michael Schuman

November 16, 2014

More from

TIME

More From TIME