In the Latest Issue

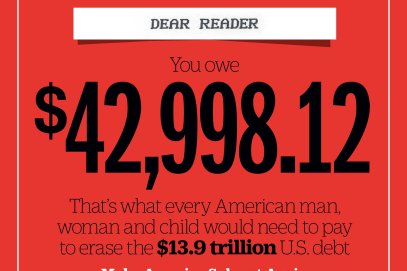

The United States of Insolvency $13,903,107,629,266. Can the nation afford this much debt?A Debt We All Must PayWhat Today’s Democrats Can Learn from Bill Clinton’s Crime and Welfare-Reform BillsHillary Clinton’s campaign could use a strong...

By TIME Staff